Delivering Great Customer Service in Banking and Finance

Whether businesses or individuals, customers have very high expectations for their financial services, and that’s for good reason. We’re giving our salaries, savings, and investments — essentially, our entire livelihoods — to institutions and entrusting them to manage those resources responsibly and safely.

Customer expectations and preferences vary, which makes delivering great customer service in banking and financial services challenging.

Here’s a quick example from my own life:

As an individual customer, my primary concern is trustworthiness. I would never sign over my paycheck to a random stranger on the street, so why would I do the same to a bank that took my money and then made it difficult to manage my funds or reach them with questions?

As a business owner, I need more than just trustworthiness. I need security and tools that inform the financial decisions I make for my company. Tools that allow me to invoice clients, pay team members, plan for and pay taxes, and manage my budget are a must. I use different banks for my personal and business funds, because my needs for each are different.

On top of that, as a customer support professional, I know that those categories break down even further: Young customers expect different things from their banks than older customers, and small businesses have different worries than enterprise companies.

Financial institutions also have their own concerns: an increasingly complex security and privacy landscape, an unpredictable economy, legal and regulatory requirements, and new and evolving financial technologies. Juggling customer needs and expectations with security and regulatory requirements can create a tough environment for providing great customer service.

That’s not to say that it’s impossible — in fact, that challenging environment is ripe with opportunities to go above and beyond to serve your customers if you’re savvy enough to recognize them.

This article will help you do just that. We’ll identify common customer service challenges in the finance and banking industries and offer tips for overcoming them.

Why great customer service is crucial in financial services

Customer experience can be a massive differentiator, and in an era of expanding financial service options, woe to any bank that doesn’t understand what its customers need or neglects to meet those needs.

Nearly 60% of Americans say that “good customer service” is the number one reason they stay with their banks. And although 89% of customers say they’re happy with their current financial institution, a significant number (37%) say they would switch to a different institution if it better aligned with their needs.

That seems to indicate that while banking customers are generally satisfied, they aren’t particularly loyal.

When customers switch banks, they rely heavily on the reputation of a financial institution when deciding on their next choice: 48% of customers say that a recommendation of a friend or family member is important when they choose a new bank, and a whopping 78% say they rely on online reviews when making their decisions.

Providing excellent financial products and excellent customer service is the secret recipe for a reputation that not only attracts customers but also retains them for years to come.

7 common customer service challenges in the finance industry

The financial industry faces unique challenges in providing excellent customer service. Companies have to manage complex rules and regulations, products, and diverse customers with differing needs and expectations, all while hiring, training, and retaining talented agents to support them.

Financial regulations and privacy

There’s no shortage of rules and regulations in the financial industry. They exist at the state, national, and international levels, and they dictate what you can say, whom you can say it to, and how you can transmit information.

The core goal of almost any regulation is to protect companies and consumers, which we all can agree is good. But that doesn’t make learning and navigating the different regulations any easier. Not only do customer service agents have to learn existing rules and regulations, but they also have to stay abreast of new and changing regulations, which can be both expensive and complicated to manage for financial services companies.

Complex products

Financial literacy is having a tough time in America: Two-thirds of Americans can’t pass a basic financial literacy test, and four in 10 say they “have no idea how credit scores work.”

This means customer service teams have their work cut out for them when helping customers with even basic financial concepts (not to mention the financial products that are so complex even financially savvy people struggle to understand them).

It’s also not unusual for customers to contact customer support about products they didn’t choose for themselves. For example, they may want to know about the 401(k) their company enrolled them in or the stock options they receive as part of their compensation package.

Articulating complex financial information in those situations can be difficult and requires specialized skill, empathy, and education from customer service agents.

Building trust with customers

Trust is paramount in any customer interaction, but it’s even more so when money is involved. However, according to an interviewee for this article who works in customer service at a finance company, “around 70% of customers say all financial advisors are crooks and liars.”

Though that’s obviously far from the truth — and purely anecdotal — it’s not the only sign of distrust. A Gallup study asked respondents to rate how honest and ethical certain professionals are, and stockbrokers ranked near the bottom of the list.

Because communicating about complex financial products with customers can be difficult and because financial institutions operate under regulations that limit the information they can share, there can be a gap between what the institution can do and what the customer understands they can do.

This lack of understanding can hinder trust-building between clients and customer service teams, which can in turn impact the customer’s desire to stay or switch to a new financial institution.

Adjusting to different customer needs

As I’ve already noted, with a wide variety of products and services comes a wide variety of customers and needs.

For example, a majority of customers age 65 and older prefer phone support over any other channel, but customers age 18-44 are twice as likely to prefer AI or live chat, and 38% are more likely to give up on solving an issue if they can’t do so with self-service.

Financial services companies must offer a variety of customer service options to support an increasingly diverse customer base.

Balancing service and selling

Some roles in finance are solely focused on customer service, and others are focused solely on sales. However, there are some — like financial advisors and loan officers — that sit somewhere in the middle of that spectrum.

They need to provide great service to retain customers, but they also usually have a component of their pay tied to signing up clients for certain products or services. Financial services have to encourage customers to take advantage of beneficial products without making them feel pressured or exploited.

Ensuring adequate staffing

Finance is a uniquely challenging industry for customer service, simply because the stakes are always high for customers.

Their money is precious; mistakes and mishandling (either theirs or the institution’s) can literally mean the difference between the customer having the basic necessities for life…or not.

Customer service agents not only need the training and experience to support complex financial products, they also need the so-called “soft skills” to work with customers through difficult conversations and situations: patience, empathy, and de-escalation skills.

Given the pressure and stress involved with providing customer service for financial services, it can be challenging for institutions to find qualified talent and retain them long term.

10 tips for improving customer service in financial services

The challenges above might seem daunting, but the following tips will help you support and develop your customer service team and offerings to meet those challenges and wow your customers.

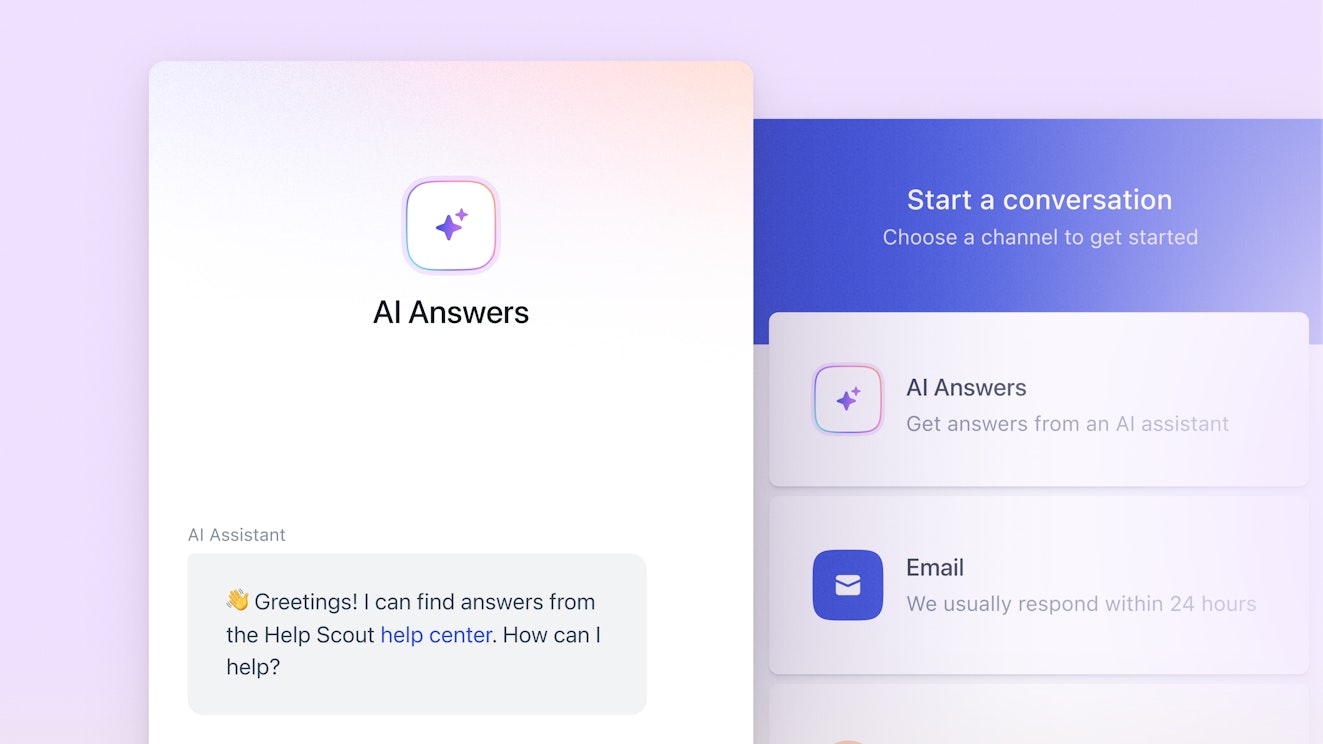

1. Use AI to meet customers’ needs

Using AI in your customer service is a fantastic way to expand your support offerings and address the varying needs of your customers (and your support team, too).

Tools like AI chatbots can detect and flag potential fraud in real time, answer increasingly complex customer questions, guide them to the right help center articles, and even provide a more personalized, human feel over the phone as they progress through your IVR system.

This is something many customers are open to: 65% say they expect some kind of AI in their interactions with financial services, and 52% cite saved time and faster resolution as the biggest benefit of using AI chatbots.

Customer support teams can see big benefits from AI as well. Having already been freed from answering simple, repetitive questions, tools like Help Scout’s AI Summarize can quickly bring agents up to speed on long, complicated threads. Features like AI Drafts can improve or fully draft responses to customers, helping agents efficiently and effectively address customer concerns.

2. Focus on real-world applications in training

Each year, companies spend lots of time, money, and energy training new and existing staff. For all the effort, we should expect some strong results, right? Well, not so much. One study by McKinsey found that only one-fourth of respondents thought training programs at their companies measurably improved performance.

There are a few things that can contribute to training being ineffective, but the largest culprit is a lack of application. We tend to learn in a classroom-like environment, where we receive information but never actually put it to use.

The problem is, studies show that if we don’t actually use what we’ve learned within six days, we forget around 75% of it.

You could have your team apply knowledge when they’re learning by creating exercises like practice client calls, where you set a basic scenario and have them play it out. It also allows you to provide real-time feedback to further refine understanding.

Recommended Reading

3. Allow your agents to specialize

Each area of finance has unique rules. Stocks and bonds are different from annuities and IRAs, and it's very difficult to be an expert in every area. If you have a large enough team, allow them to build their expertise in one or two areas so they can provide outstanding support for their products and services.

If that's not possible, consider rotating each agent through providing support for each product. For example, you could have agents work on practice cases for one product type for a week, then switch to a different product type the following week.

Breaking information into smaller pieces and allowing agents to focus on one area at a time for an extended period will help them learn and retain more information. You can also quiz them at the end of each rotation — research shows quizzes can help with information retention — and have a real-world exercise to make sure they’re grasping the information.

4. Provide ongoing training

It’s common for financial regulations and laws to change, making retraining necessary. Though there may be some lead time, regulation changes aren’t generally headline news, so you do need someone paying close attention to track and report any upcoming changes.

In addition to training on new rules or regulations, you should also set up a regular cadence for refresher courses. Certain certifications and regulations require this, but generally only once every few years, which probably isn’t often enough.

Consider doing short classes every six months or so. That frequency shouldn’t be too disruptive, and it gives an opportunity for people to apply knowledge. You could even survey reps ahead of time to ask which areas they’re less certain about, and focus on those.

5. Let customers lead the conversation

It’s not always necessary to cover every aspect when talking with a client. Start with a high-level overview, then get into specifics as needed for each case. Rushing into the nitty-gritty too quickly can intimidate some people.

You could also simply ask how detailed they want you to get with an explanation, so you know from the start where they’re coming from. Remember, the types of questions they ask could signal their knowledge level.

No matter what, at the end of any explanation, ask if they need further clarification on any point or have any further questions to make sure they get all the information they need.

Also, don’t expect customers to understand everything right away (remember how long it takes you to learn a product!). Be prepared for multiple follow-ups and ready to answer the same questions repeatedly. Create a great knowledge base with self-service resources so customers have an option for self-directed learning.

Wherever possible, consider making plain-language explanations of your different products. Removing jargon and legalese can make information easier to digest for someone without a finance background.

Recommended Reading

6. Be as transparent as possible

A lot of distrust between customers and financial companies comes from the impression that information is being withheld. Due to the nature of financial services, there are certain things you simply won’t be able to say. Though you may not purposefully be opaque, if you’re not mindful, it could easily appear that way to a client.

For example, if a client asks what return they can expect on a certain fund or stock, there’s no way for you to accurately predict that because no one really knows. However, you could present historical data and be open about where your predictions come from.

Another area you can be open about is fees. You could even write an article covering common fees, where they come from, and how they’re assessed. In the case where there’s information you can’t share, you need to be even more articulate as to why you’re not able to.

7. Set expectations early

Since finance is so competitive, it’s common to lead with best-case scenarios for things like rates and returns. Though that may be a good tactic to get someone through the door, if they don’t get what was advertised, it can cause trouble.

When talking with clients, be very upfront about what they can realistically expect from a product or service. For example, if they’re applying for a loan, let them know that only those with near-perfect credit tend to qualify for the lowest rates.

Also, set expectations early about what you can do for them in your specific role. For example, you might not be able to offer advice or give direct product recommendations. Being honest from the start means there won’t be any surprises for the client, which helps build a foundation of trust.

8. Communicate proactively

Personal finances tend to be a touchy topic. It’s an area where people fundamentally want only good news, and even neutral news can feel like a huge letdown — all of which makes communicating information potentially uncomfortable.

Keeping clients in the loop without them reaching out first can signal that you don’t have anything to hide and can help build trust. Whether it’s good or bad news, tell them ASAP — it’ll serve you best in the long run.

In fact, one study found that people prefer hearing bad news first then good news afterward (though the study also reports that those telling the news tend to prefer leading with the good).

Recommended Reading

9. Focus on consulting, not convincing

We’re all familiar with the cliche of fast-talking salespeople who’ll stop at nothing to close a deal. At the core of the cliche is always someone who is completely and totally motivated by their own self-interest.

Selling in a “do whatever it takes” manner can produce short-term results but hardly ever works in the long term. The primary reason is that once someone figures it out, they don’t trust you anymore, and if they don’t trust you, they won’t do business with you.

Many modern companies — and salespeople — have started taking a consultative approach. Instead of trying to force an agenda, they take time to get to know their clients and to learn their goals and needs. Based on that information, they can make relevant and helpful recommendations.

For example, if you’re a financial advisor, you could have prospective and current clients complete a short questionnaire to better understand their goals and tailor future communication to those goals.

It’s also important to recognize that selling and service both take a decent bit of time. If some part of your team’s pay or performance metrics is tied to sales, it can be hard for them to justify time away from selling activities. There will always be some tension between the two, but there are ways to ease that tension.

The best way to achieve this is to align sales and service goals. For example, if you conduct customer satisfaction surveys, you could award bonuses, extra vacation time, or similar rewards to those with the highest ratings in a quarter.

You could also consider raising the commission rate for agents who retain customers longer. For example, let’s say you pay advisors 0.5% of assets under management (AUM). You could create a sliding scale in which, after a client has been with an advisor for 5+ years, the rate for that account moves to 0.7% AUM.

Providing the incentive does two things: First, it shows that it’s a business priority, which is powerful in itself. Second, it could help ease any worry staff have about spending extra time on service and taking some time away from selling.

10. Invest in your team’s careers

If you look at almost any list of the highest turnover positions, customer support is always near the top. Though there are many reasons for that, the lack of company investment in the agents’ careers is often a major contributing factor. Leaders can mitigate this by offering customer service teams additional skills training and by defining clear career paths.

In one study, nearly 20% of millennials listed additional skills training among the top three benefits they were interested in, along with paid time off and flexible working hours.

If you know an agent is interested in learning more technical skills, you might be able to get them plugged in by working more closely with your engineering team. Or perhaps they want to work toward an HR career path: You could get them involved in team hiring or onboarding.

Through that exposure, support professionals may find an area within — or outside of — support that piques their interest and that they’d like to explore further. Providing opportunities to do that can be a great way to help further develop skills and keep them around for the long term.

This is where building out a career path plan becomes important. This looks different for every team, but there are two things you should focus on:

Clarity: Having clear-cut markers and milestones for people to achieve and aspire to are critical to measure where they’re at. For example, you might have someone lead a project as they work toward leading a team.

Flexibility: It’s easy to think about career paths only as they relate to the area of the business someone is currently in, but it’s possible they may want to grow into a different discipline, so you need to account for that. You can also create paths for people who want to become people managers as well as individual contributors. Both are key to your business's success.

There may not always be a perfect fit right away. Be sure you’re keeping track of people’s interests, continue looking for opportunities on their behalf, and encourage them to bring their own ideas to the table.

If you’d like to learn more about customer service career paths, check out how we approach them on our support team here at Help Scout.

Investing for the long term

There are certainly challenges when it comes to delivering a great customer experience in the financial industry, but it’s absolutely possible to do so. As long as you’re being proactive and present, you’re on the right track.

Just as it is in finance, there aren’t any shortcuts to delivering great service — it takes time, energy, and commitment. But when you do commit to providing great service, you’ll find it’s an investment that pays dividends for years to come.

Steph Lundberg

Steph is a writer and fractional Customer Support leader and consultant. When she’s not screaming into the void for catharsis, you can find her crafting, hanging with her kids, or spending entirely too much time on Tumblr.

Jesse Short

After spending a few years working as a support agent, Jesse made the switch to writing full-time. He is a Help Scout alum, where he worked to help improve the agent and customer experience.